BY GARY BENDER

The U.S. industrial gas industry is approaching a supply inflection point that has received little attention. While hydrogen’s role in clean energy and mobility continues to dominate industry conversation, a more immediate and structurally significant disruption is already in motion along the Gulf Coast. It is one that will reach independent distributors before most have had time to prepare.

The return of Venezuelan heavy sour crude to U.S. refineries is not a projected scenario. Crude flow is already increasing and is among the heaviest processed in Gulf Coast facilities. It requires 17 to 20 pounds of hydrogen per barrel. This is roughly 10 to 20 times the demand of domestic light crude. For the last five years, the U.S. has been processing 340,000 barrels of Venezuelan oil per day. When that volume approaches the expected one million barrels per day, a level consistent with historical Venezuelan imports, the resulting increase in hydrogen demand does not strain the system. It breaks it.

What makes this particularly consequential for the distributed gas market is where independent distributors sit in the hydrogen supply hierarchy. Most distributors operate under the reasonable assumption that supply will remain accessible, even if it becomes more expensive or is subject to occasional delays. That assumption reflects past conditions. What Venezuelan crude onshoring introduces is a structural shift in demand priority. It is one in which distributors will find supply increasingly difficult to secure and at substantially higher costs, not because of temporary market fluctuations, but because of where they rank when allocation decisions are made. (This has nothing to do with the recent and hopefully temporary supply and cost issues related to the Middle East battles.)

THE INFRASTRUCTURE HAS NO RESERVE

The Gulf Coast hydrogen pipeline network operates at 95% utilization today (higher than preferred). There is no buffer. The 600-mile system connects 22 gaseous hydrogen plants to contracted mega refinery customers like Exxon, Chevron, Marathon, Valero, Phillips 66, and others. When refineries need more, the pipeline redirects molecules from wherever they can be pulled.

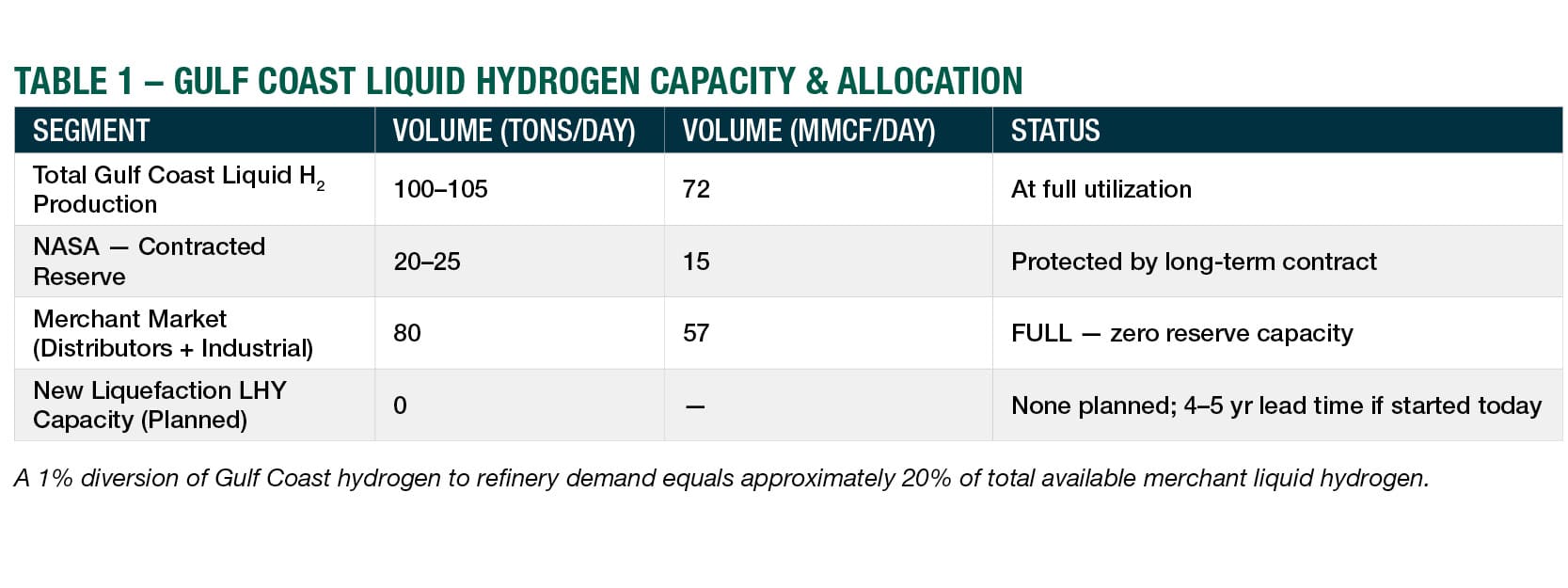

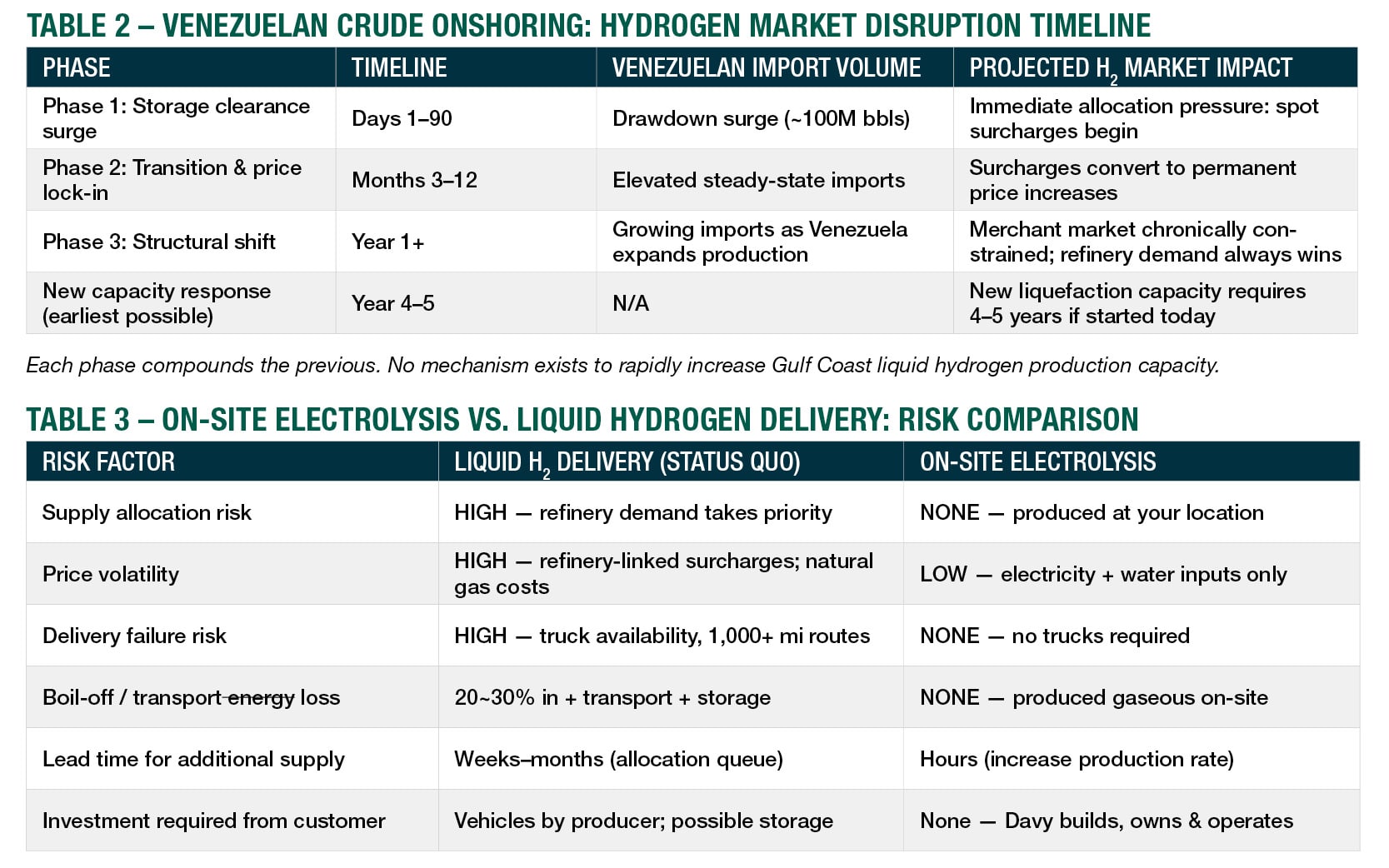

The liquid hydrogen picture is equally constrained. Total Gulf Coast liquid production capacity is 105 tons per day. About 20% is contractually protected for NASA. The remaining 80 tons per day serve the entire merchant market which includes every distributor and industrial user across the South, Mid-Atlantic, and Eastern U.S. That capacity is fully utilized. No new liquid hydrogen plants are planned, and any expansion started today would take four to five years to reach production if they can find available land on a natural gas pipeline with a long-term supply.

THE MATHEMATICS OF DISRUPTION

The numbers are unambiguous. Venezuelan crude processing at one million barrels per day generates demand for an additional 17 to 20 million pounds of hydrogen daily which is roughly 8,500 additional tons per day. Even accounting for on-site refinery hydrogen generation, any incremental refinery demand will draw from the same pipeline and merchant supply that distributors and their customers depend on.

The disruption unfolds in phases. Venezuela must first clear approximately 100 million barrels from existing storage to sustain continuous exports. This process is underway and is expected to take 90 to 120 days. That initial surge creates immediate allocation pressure. As exports stabilize at elevated levels (one million barrels per day) and Venezuela’s production capacity continues to recover, imports to U.S. refineries will grow accordingly. Temporary surcharges become permanent price increases. The window for acting ahead of this is measured in months.

WHO GETS CUT AND IN WHAT ORDER?

In every prior industrial gas supply disruption, independent distributors were cut first. Venezuelan crude onshoring converts this historical pattern into a structural condition.

The allocation hierarchy in a tightening hydrogen market is not speculative. It is established by contract, infrastructure, and precedent. NASA’s supply is protected. Large industrial customers with multi-gas long-term agreements, steel companies, semiconductor manufacturers, and utility turbine operators have supply security through existing huge contracts although prices will likely increase. Independent distributors do not have the leverage for supply or price.

The downstream consequences extend well beyond surcharges and price increases. The ”smaller” liquid hydrogen users: annealing operations, food processors, specialty metal manufacturers, and automotive alloy producers will face operational disruption. Hydrogen-powered forklift fleets at major distribution centers face the same constraint disruption. Independent distributors will face supply and cost pressure and pressure from distributors aligned or owned by the major corporations who produce hydrogen. Hydrogen will become a strategic differentiator, meaning accounts that need hydrogen will be at risk if the distributor’s supply or costs become volatile. Hydrogen has no substitute, and there are few suppliers who are able to pivot even in normal times. There is no rapid alternative.

THE CASE FOR REGIONAL PRODUCTION

Transportation, storage, and liquefaction already account for up to 50% of hydrogen’s final delivered cost. When allocation risk and surcharges are added on top of that, the economics of distributed production shift decisively.

Regional facilities sited at distributor transfills or large user locations eliminate supply concerns, boil-off losses, transportation costs, price volatility, and allocation exposure. This converts hydrogen from a supply liability into a controlled cost and a competitive advantage.

On-site production is no longer an experiment; it is established technology that can be deployed at scale. For distributors who depend on reliable hydrogen access, it will become a risk management decision. In the past, onsite production required significant investment and unique production skills that few distributors possess. For most, those barriers remain.

The alternative is an onsite partnership with Davy Gas. Davy owns and operates the plant on a long-term basis and locates the plant at the user’s location. The oxygen co-product is captured allowing high purity oxygen to be provided to the transfill or specialty gas plant, thus reducing purchases, and providing the high purity oxygen needed for some accounts and for some specialty gas mixes.

Whether a distributor chooses to invest in and operate a hydrogen plant or partners with Davy, they will be in a fundamentally different competitive position than those waiting for merchant allocation. In a market where refinery demand structurally displaces distributor supply and prices are increasing and volatile, that position is not a strategic luxury. It is operational continuity and a necessity.

Gary Bender is Chief Development Officer at Davy Gas Inc., specializing in modular hydrogen/oxygen production systems designed for distributed applications. Learn more at davygas.com.

About Davy Gas Inc.

Davy Gas builds, owns, and operates modular on-site hydrogen and ultra-high purity oxygen production systems at customer locations — with zero upfront investment required. Serving independent gas distributors, steel manufacturers, data center operators, and logistics fleets across the $6–8 billion distributed hydrogen market.